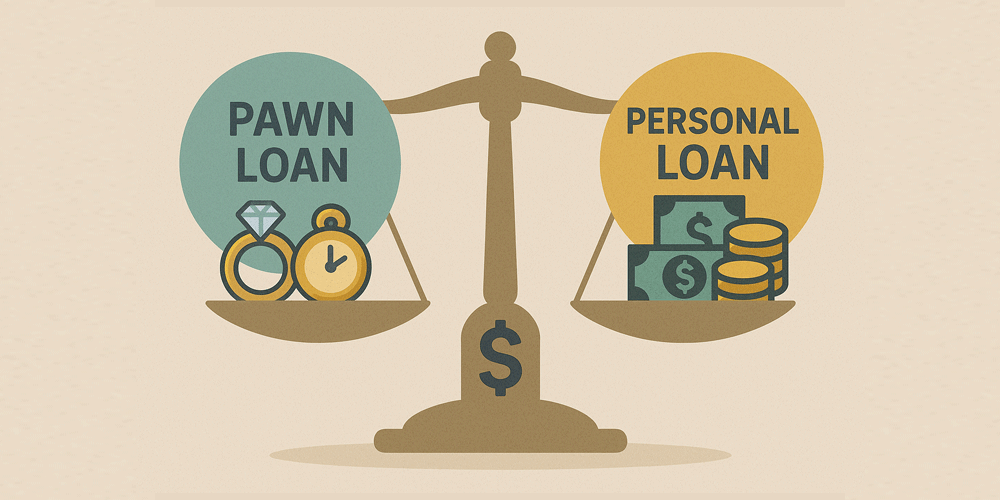

Pawn Loan vs Personal Loan: Which Is Better for Quick Cash?

When life hits you with unexpected expenses—a car repair, medical bill, or rent due date—accessing cash fast becomes your top priority. Two common options many people consider are pawn loans and personal loans. But which one is better for quick cash, especially if your credit isn’t great or you need money right away?

This guide breaks down the differences between pawn loans and personal loans, compares their pros and cons, and helps you decide which short-term borrowing option makes the most sense for your situation.

What Is a Pawn Loan?

A pawn loan is a short-term, collateral-based loan you get from a pawnshop. You bring in an item of value—like gold jewelry, a Rolex watch, or an electric guitar—and the pawnbroker lends you a percentage of its resale value. If you repay the loan (plus interest and fees) within the agreed time, you get your item back. If not, the pawnshop keeps and sells your item. There’s no credit check, and the process is fast—usually under 30 minutes.

Need Quick Cash? Let's Talk Pawn Loans.

Have Jewelry you'd like to leverage for a short-term loan? We're here to help. No credit checks—just honest, fast cash offers.

Call Now - 954-923-2372What Is a Personal Loan?

A personal loan is an unsecured loan typically offered by banks, credit unions, and online lenders. You borrow a fixed amount—anywhere from $500 to $50,000—based on your credit score, income, and financial history. You repay it in fixed monthly payments over time, usually 6 months to 5 years. Approval depends heavily on your creditworthiness, and funds are typically deposited into your bank account in 1–3 business days.

Quick Comparison Table: Pawn Loan vs Personal Loan

| Feature | Pawn Loan | Personal Loan |

|---|---|---|

| Credit Check | No | Yes |

| Collateral Required | Yes | No (typically) |

| Loan Amount | $50–$2,500 (avg) | $500–$50,000+ |

| Approval Time | Within minutes | 1–3 days (sometimes same-day) |

| Repayment Period | 30–90 days | 6–60 months |

| Risk if Unpaid | Lose the item | Collections, credit damage |

| Impact on Credit | None | Yes—positive or negative |

Speed: Which Loan Gets You Money Faster?

If your priority is speed, pawn loans are tough to beat. Walk into a pawnshop with your item, get an appraisal, and walk out with cash—often in 15–30 minutes. There’s no application, underwriting, or banking delay. Personal loans, on the other hand, can take hours or days, depending on the lender and whether additional documentation is required.

Winner for speed: Pawn loan.

Approval: Can You Get the Loan Easily?

Pawn loans have virtually no barriers to approval. You don’t need good credit, income verification, or even a bank account. If your item has value, you’ll get a loan. Personal loans, however, usually require a credit score of 600 or higher. Borrowers with poor credit may be denied or only qualify for small amounts at high interest rates.

Winner for accessibility: Pawn loan.

Loan Amount: How Much Can You Borrow?

Personal loans typically allow for larger borrowing amounts—from a few hundred dollars up to tens of thousands, depending on your credit and income. Pawn loans are limited by the value of your collateral.

Winner for smaller loan amounts: Pawn loan.

Risk and Consequences of Default

With a pawn loan, if you don’t repay, the pawnshop keeps your item. You don’t owe anything else, and your credit score remains untouched. With a personal loan, defaulting can wreck your credit, lead to debt collections, and even result in legal action. You’re personally liable for the full repayment.

Winner for lower risk: Pawn loan.

Repayment Terms and Flexibility

Personal loans have set monthly payments and longer terms—often 12 to 60 months. This predictability is useful if you have a steady income. Pawn loans have shorter terms (usually 30–90 days), but they may allow rollovers or extensions by paying just the interest. However, repeated rollovers can rack up high fees.

Winner for short-term flexibility: Pawn loan

Who Should Choose a Pawn Loan?

- You need cash immediately

- You have poor or no credit

- You don’t want debt on your credit report

- You’re okay parting with the item if needed

- You’re borrowing a small amount

Who Should Choose a Personal Loan?

- You have fair to good credit

- You need to borrow a large sum

- You want predictable monthly payments

- You’re not comfortable putting up personal items as collateral

- You need more time to repay

Which Loan Is Right for You?

If you’re in a credit crunch and need quick cash without strings attached, a pawn loan may be your best option. It’s fast, credit-free, and low-risk in terms of debt obligations. However, you’re limited by your item’s value, and fees can stack up fast.

If you have really good credit and need a larger loan with repayment terms over longer period of time, a personal loan may make more sense.

Bottom line: Choose the loan that fits your timeframe, financial condition, and risk tolerance. If in doubt, speak with both a lender and a pawnbroker before deciding.

FAQs: Pawn Loan vs Personal Loan

Is a pawn loan better than a personal loan for emergencies?

If you need cash immediately and don’t have good credit, yes—a pawn loan can be the fastest and most accessible option.

Can a personal loan hurt my credit?

Yes. Missing payments or defaulting will hurt your credit. But on-time payments can improve your credit over time.

How much can I borrow with a pawn loan?

It depends on your item’s resale value. Most pawnshops offer a decent percentage of what they believe they can resell the item for.

Are pawn loans safe?

Yes, as long as you understand the terms. You risk losing your item, but not your credit or legal standing.

Can I repay a pawn loan early?

Yes. Most pawnshops allow early repayment and may even prorate the interest and fees in some cases.

Conclusion: Think Before You Borrow

When deciding between a pawn loan and a personal loan, it’s not about which one is universally “better”—it’s about which one is better for you. Do you value speed, simplicity, and no credit check? Then the pawn loan is for you.